The Billion-Dollar Founder Study

What 20 years of exits actually say about founding teams

Startup mythology tells us great companies are born from chemistry: college roommates, former coworkers, best friends who “just get each other.” It tells us school pedigree matters. That youth is an advantage. That brilliance is individual.

Everyone accepts these ideas at face value, but no one has built a real dataset to answer whether the conventional wisdom holds. So we did.

We set out to answer one question: what do the founding teams of billion-dollar technology companies actually have in common?

To find out, we built a dataset of every U.S. tech company that either went public or was acquired for more than $1 billion in the past 20 years, adjusting for inflation (see methodology).

What we found challenges industry mythology. Familiarity between co-founders is overrated. School pedigree isn’t destiny. And many of the assumptions founders and VCs make about what leads to big outcomes don’t hold up in the data.

But getting to those answers required reconstructing how these companies were actually formed. The real founding story is rarely written about accurately, or summarized well by AI.

That meant manually reviewing more than 2,000 LinkedIn profiles, listening to countless podcast interviews, watching old conference talks, digging through blog posts, and piecing together founding stories scattered across the internet.

For each company, we reconstructed the formation of the team from scratch, all in the pursuit of learning what patterns actually show up in venture-scale companies that make it to billion-dollar-plus exits:

- How many founders were there?

- Did they know each other before starting the company?

- Had they worked together?

- Gone to school together?

- How old were they at founding?

- Did the CEO have prior startup experience?

- What school did the founders go to?

The numbers tell a clear story: the biggest exits aren’t built by the most convenient team. They’re built by the right team, at the right time.

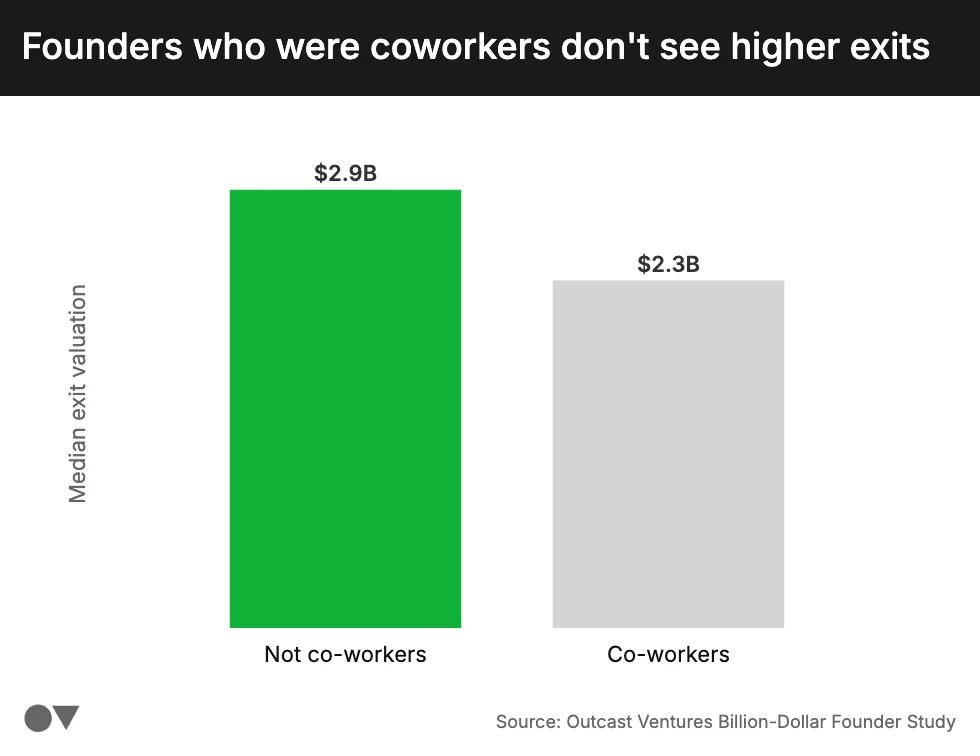

Working together before doesn’t mean a bigger exit

One of the most persistent beliefs in choosing a co-founder is that history de-risks the partnership whether it comes from working together at a former company, building context through friendship, or even ideating as college roommates. The story feels safe because trust is seemingly built.

But longer relationship histories don’t translate into larger exits. When founders had worked together before, the median exit valuation was $2.3B, lower than the $2.9B median for those who had not. That’s a 26% gap in median exit valuation.

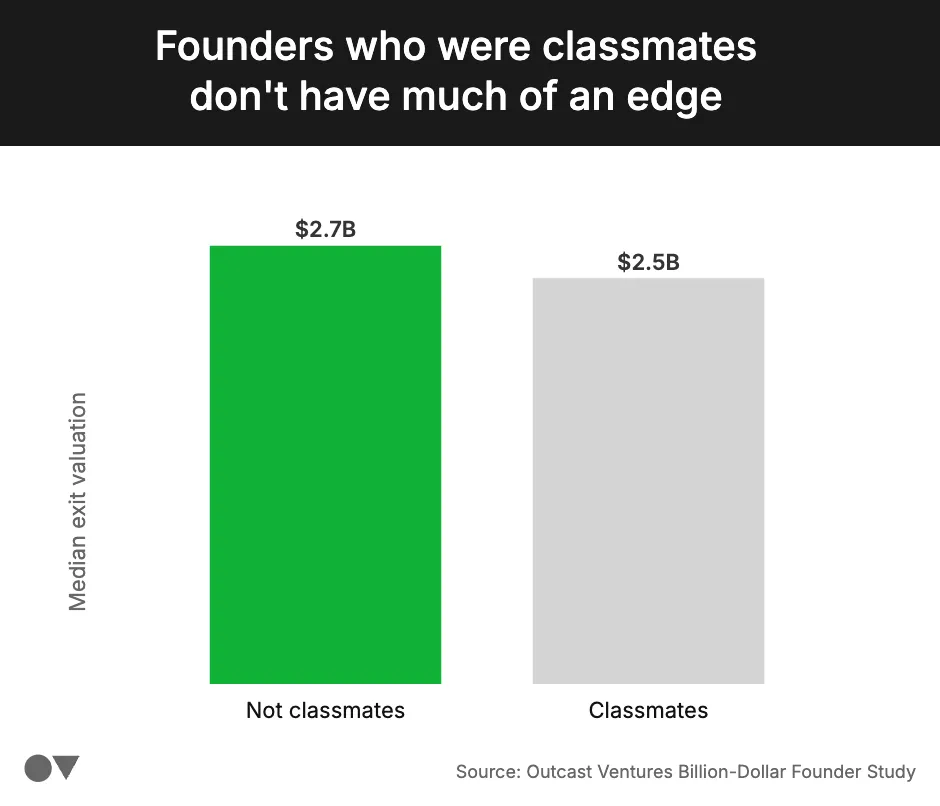

And the pattern repeats with school ties. Founders who went to school together show a slightly lower median valuation ($2.5B) than those who did not ($2.7B).

This doesn’t mean prior relationships are a liability, but they are far less of an advantage than many assume. Shared history reduces friction early on, but the real test comes later because scale is not won in the first six months.

The best co-founder isn’t the most convenient one. It’s the most complementary one.

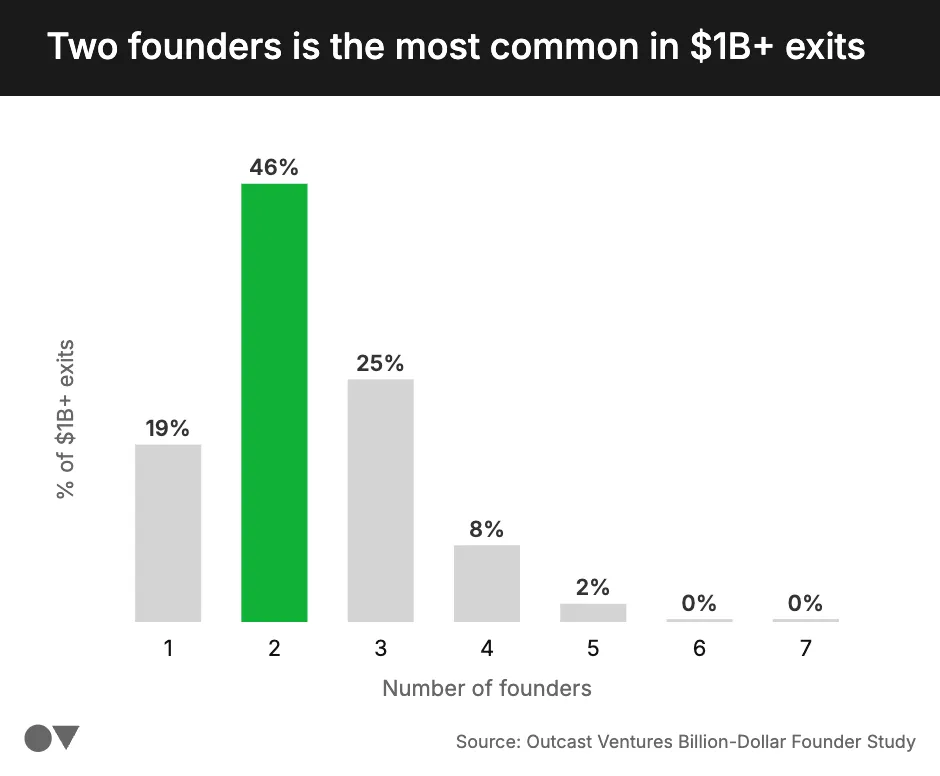

Teams outperform solo founders in top exits

When looking at the companies that exited at $1B+, 82% were founded by two or more co-founders. Two founders is the most common structure. Three-founder teams are also well represented.

So yes, solo founders show up. Roughly one in five billion-dollar exits was started by a single person.

Peter Walker’s data at Carta shows that solo founding has exploded at the formation stage — rising from 18% of new startups in 2016 to 36% in 2025, accelerating sharply after the launch of ChatGPT. Solo founders are starting more companies than ever.

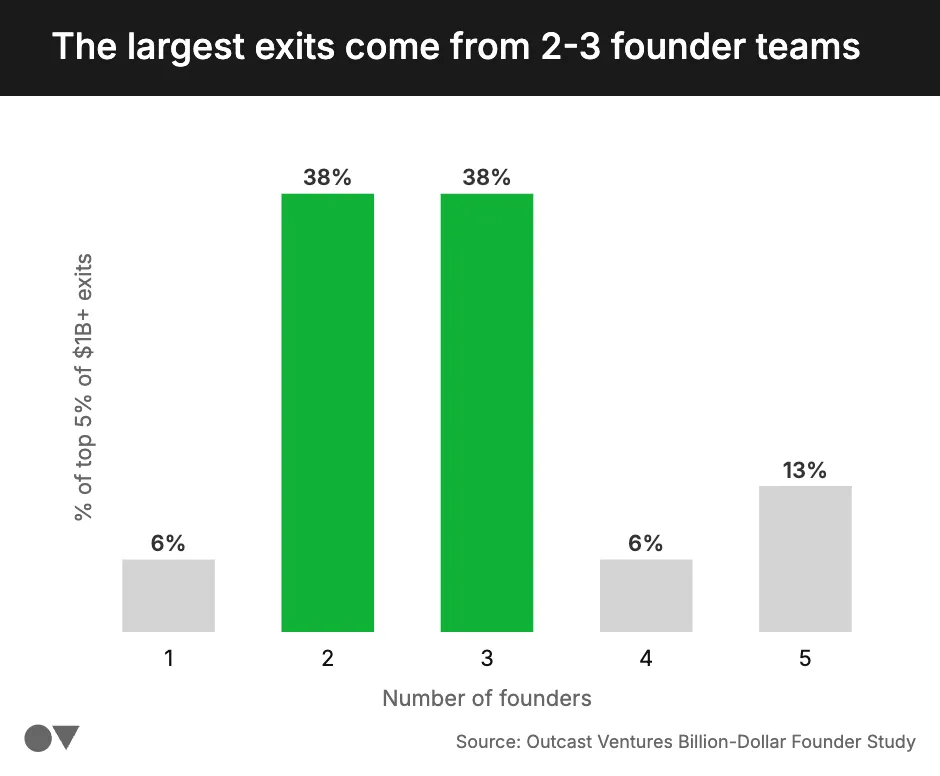

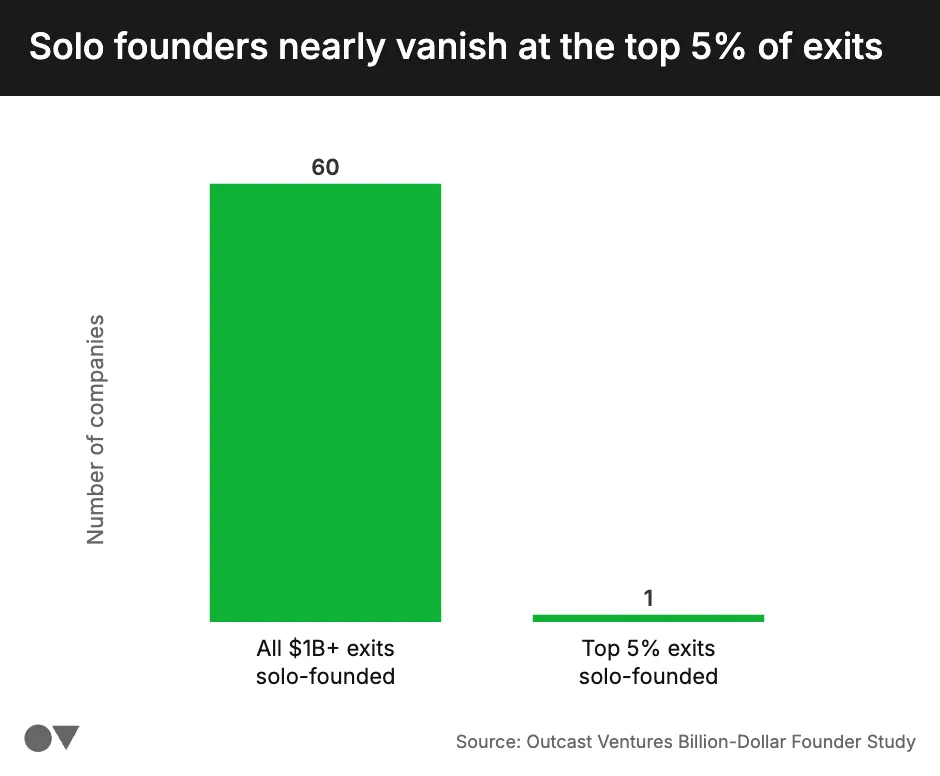

But when you isolate the very largest exits, solo founders almost disappear.

Among the top 5% of exits in our dataset – 16 companies valued between $24B and $98B – only one was led by a solo founder.

Solo founders can absolutely build valuable companies. But the largest exits overwhelmingly come from teams.

The challenge isn’t starting a company; it’s sustaining one. The companies in our dataset took a median of roughly 12 years to reach liquidity. Over that time, complexity compounds, markets shift, teams scale, and pressure increases.

The biggest edge is startup experience (and past success)

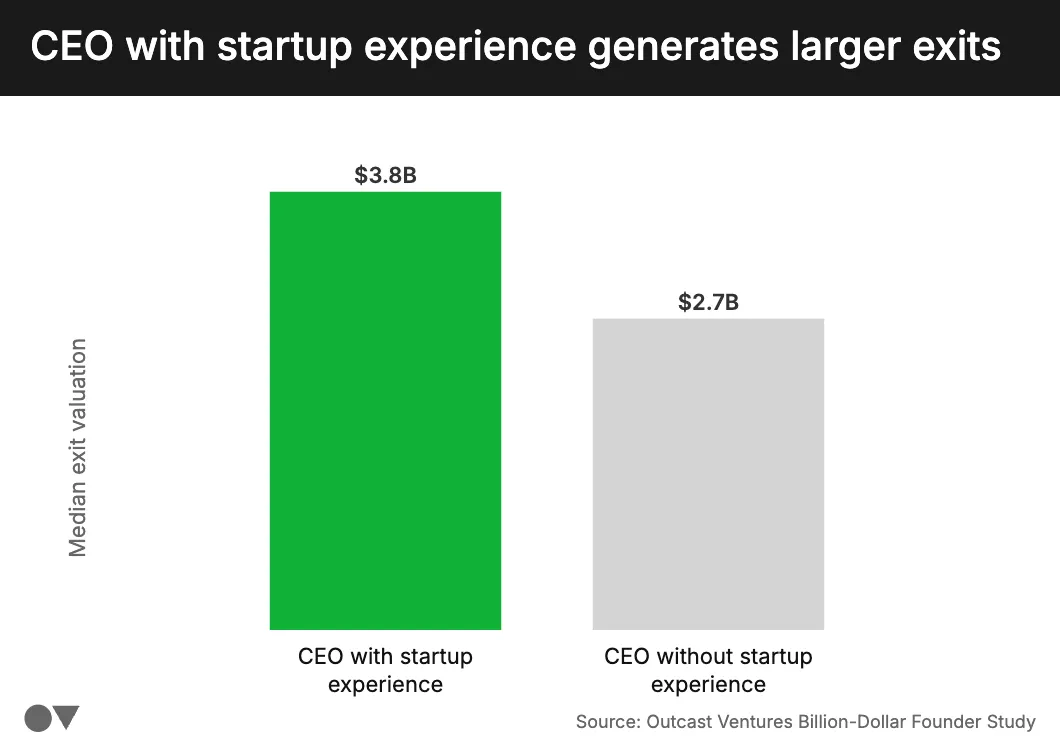

Prior startup experience, especially for the CEO, is one of the clearest signals associated with larger exits.

Among IPO companies in particular, CEOs with prior startup experience had a median valuation of $3.8B compared to $2.7B for those without, a 41% premium.

When the lens expands from the CEO to the founding team, the signal gets stronger.

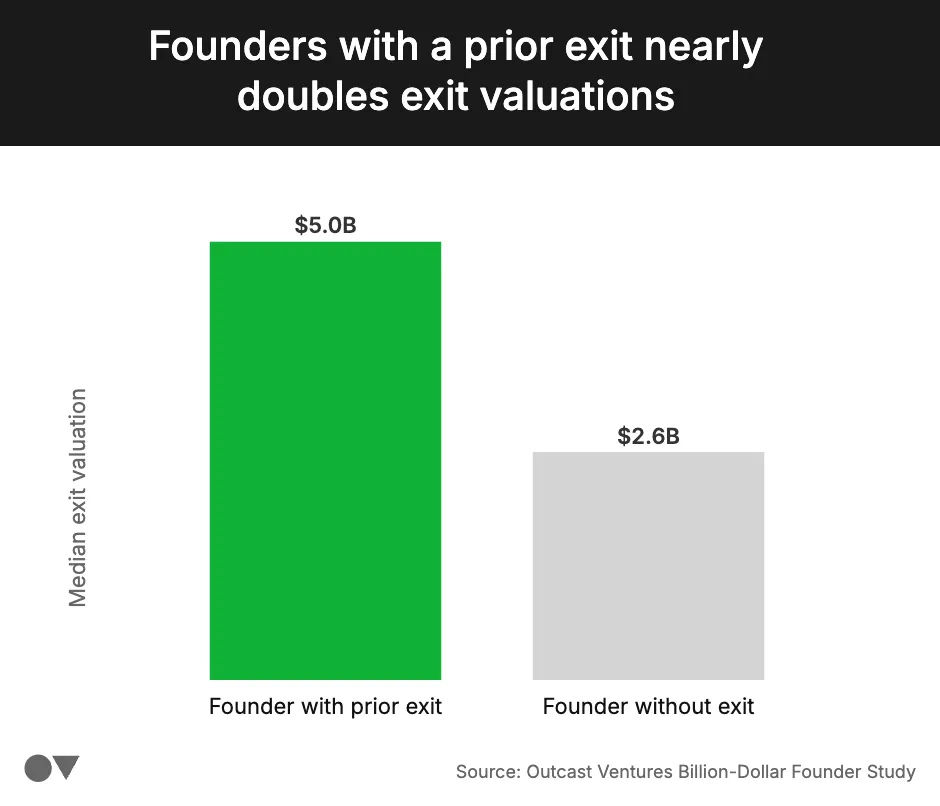

Among IPO outcomes in the dataset, teams where at least one founder had previously built and exited a company had a median IPO valuation of $5B, nearly double the $2.6B for teams with no prior exits.

Why? Scaling a company is a learned skill. Hiring at pace, managing governance, navigating capital markets, and handling board dynamics – founders who’ve done it before recognize the patterns faster. Prior exits also create personal liquidity, allowing founders to take bigger swings and focus on building long-lasting companies, rather than making safer decisions that lead to smaller outcomes.

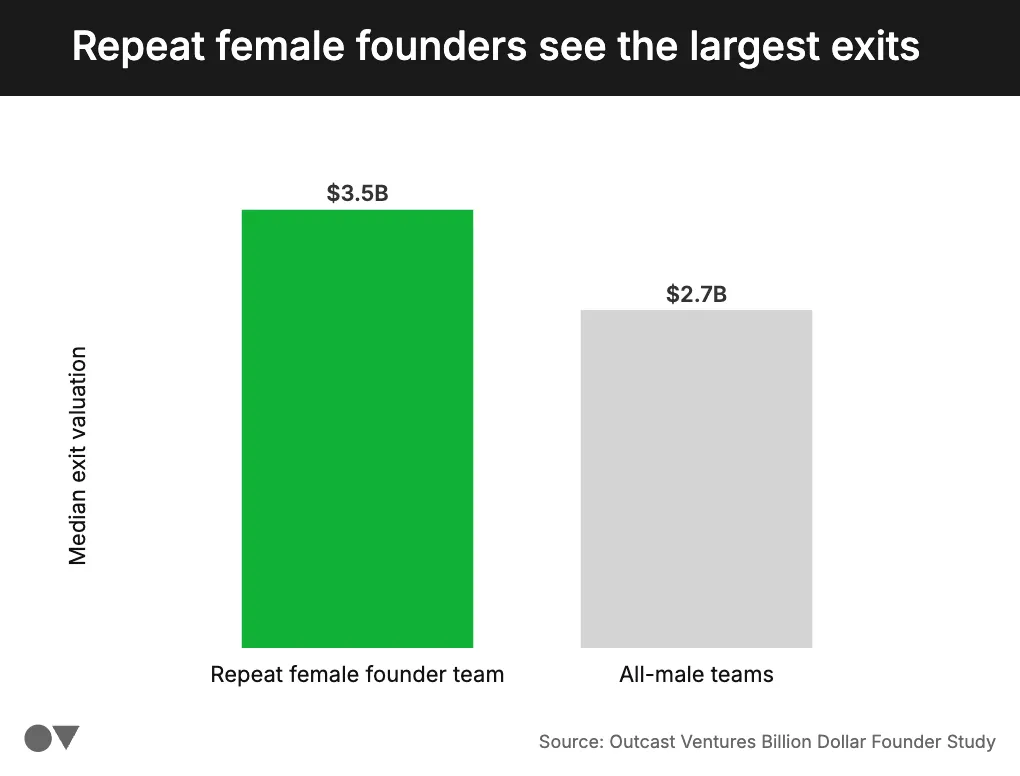

The experience advantage holds across team composition. 7% of billion-dollar exits in our dataset included a female founder. Experienced female CEOs had the highest median exit of any group — $3.5B, 30% above experienced all-male teams at $2.7B.

The fact that the experience premium appears regardless of team composition suggests it’s one of the most robust patterns in the data.

Building big takes more than a decade

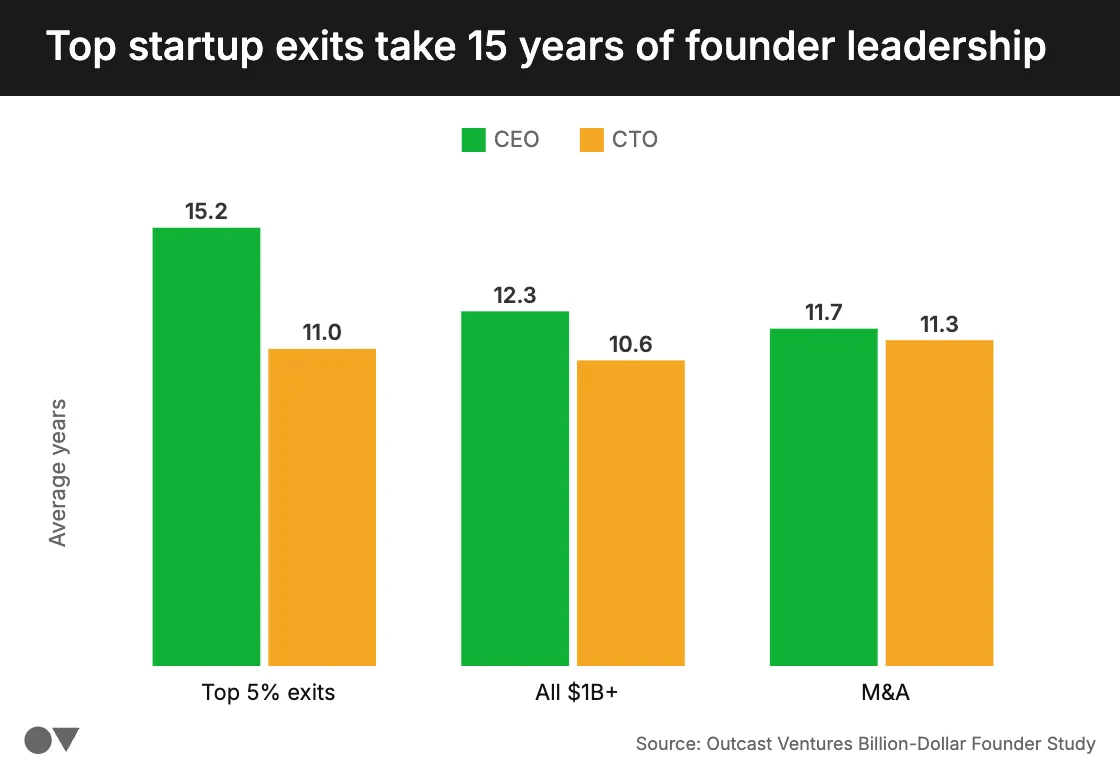

Across all billion-dollar exits in the dataset, founding CEOs stayed in the role for roughly 12 years. Founding CTOs stayed about 11 years.

In M&A exits, tenure is similar, where founding CEOs stay closer to 12 years, and CTOs slightly less than that. Acquisitions tend to happen earlier, and leadership transitions are more common before exit.

In the top 5% of exits, tenure stretches longer. Founding CEOs often stay 15+ years, with CTOs just behind them.

The trend is clear:

-

M&A exits: founding CEOs stay about 12 years, CTOs about 11.

-

All $1B+ exits: CEOs stay 12.3 years, CTOs 10.6.

-

Top 5% exits: CEOs stay 15+ years, CTOs 11.

Over roughly a decade, companies scale from dozens of employees to hundreds or thousands. They move through multiple product generations, and survive capital cycles and competitive waves that didn’t exist at founding.

If the median path to a billion-dollar exit is more than a decade, and the largest exits take even longer, you are not choosing someone to survive the launch.

You are choosing someone to build with through reinvention.

Billion-Dollar Founders are 35 years old. But timing matters more.

Startup culture celebrates youth. The numbers tell a different story.

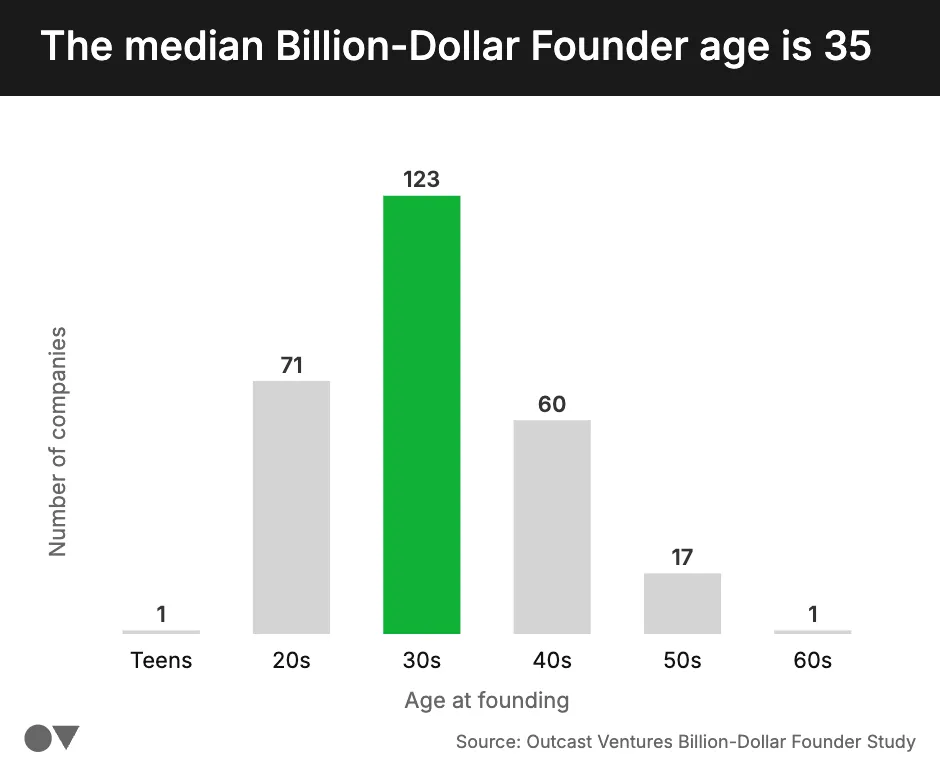

Across billion-dollar exits, the median age at founding for the primary founder is 35. These founders are old enough to have accumulated real experience, but young enough to take risks and endure a decade-long build.

Others have found the same pattern: Ali Tamaseb’s analysis of 30,000 data points on billion-dollar startups found a median founder age of 34. Aileen Lee found it the same when she coined the term “unicorn” in 2013 and again when she revisited the data a decade later. Mid-30s appears to be one of the most stable patterns in venture-scale outcomes.

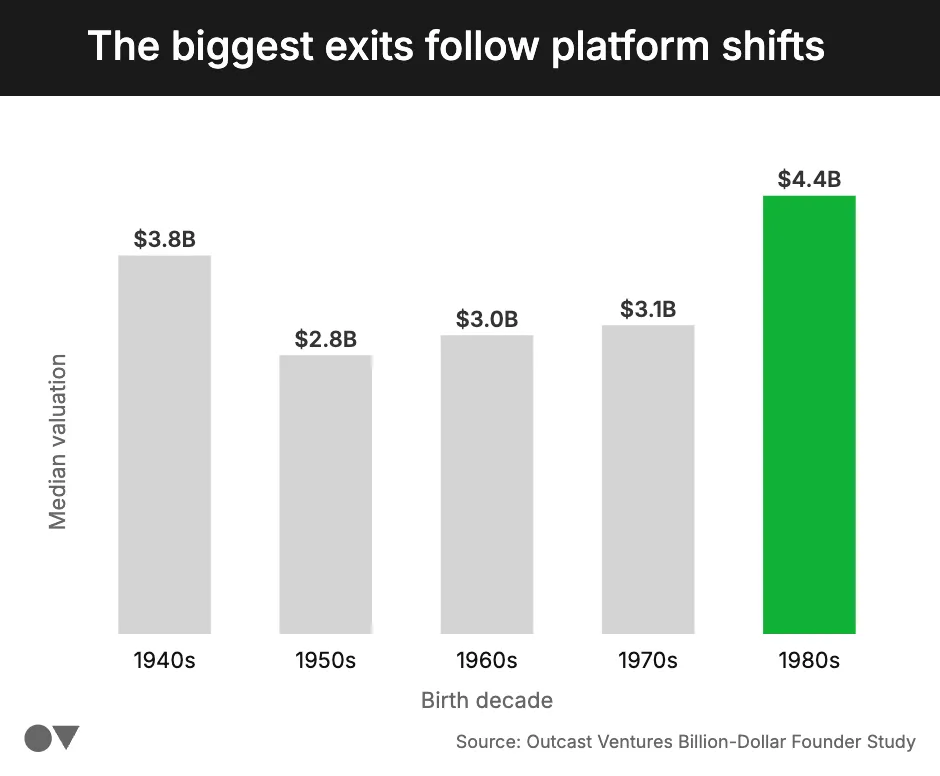

But the more interesting signal isn’t age in isolation, it’s when they were born.

When you look at IPO exits by CEO birth decade, founders born in the 1980s show up much more in the largest IPO-scale exits.

Our data suggests something different: it’s not that founders are aging into success; it’s that each generation of builders hits their prime during a different platform shift.

That cohort grew up alongside personal computing, entered adulthood during the rise of the internet, and reached prime founding age during mobile and cloud. They were well-timed, not just talented.

The biggest exits aren’t about a founder’s age. They happen when a founder reaches their prime at the moment of a major platform shift. Which raises a natural question…

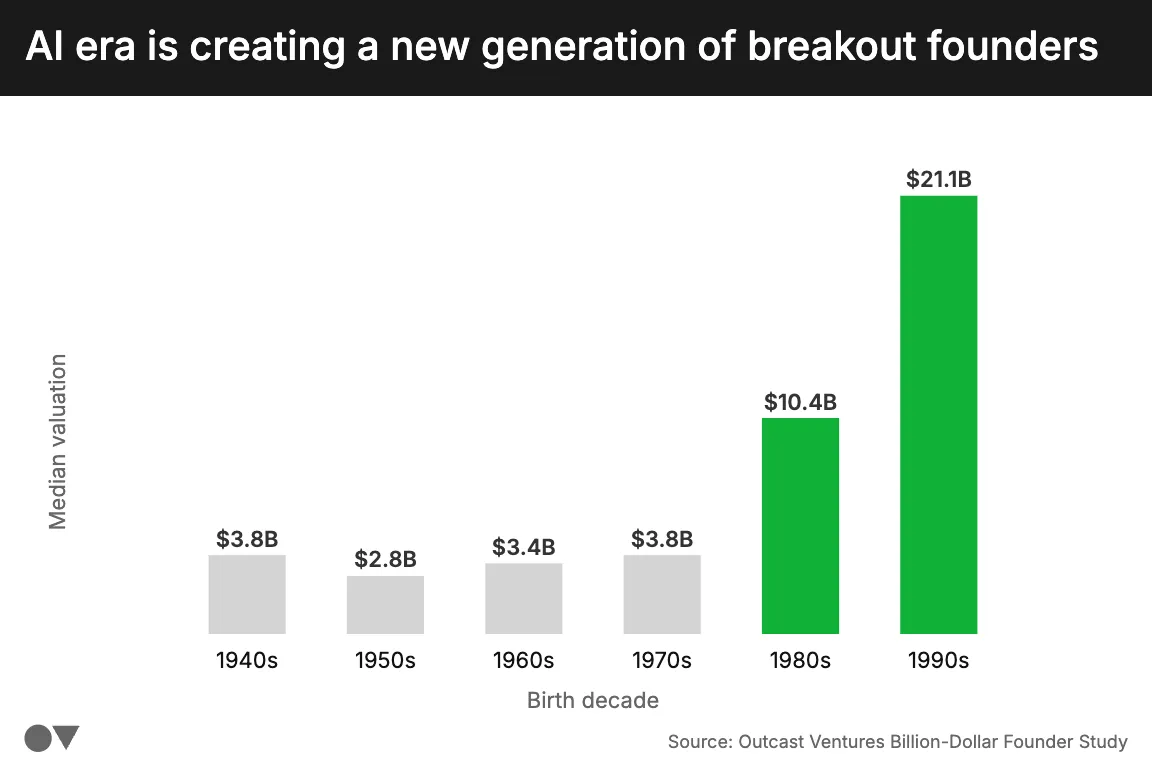

The AI Generation: Founders born in the 1990s

If the 1980s cohort rode cloud and mobile to much larger IPO, what happens to the cohort reaching prime founding age during AI?

To explore that question, we expanded the dataset. In addition to IPOs and acquisitions, we looked at the top 20 most valuable private companies in the U.S. today and incorporated their current valuations as a proxy for eventual IPO outcomes. These companies were largely built during the rise of AI and modern cloud infrastructure.

When those companies are added to the analysis, founders born in the 1990s show a sharp jump in median valuation.

The sample size is still small, so it would be premature to draw hard conclusions. But the signal is directionally consistent with what the earlier cohorts show. Notably, there is only one private company in the dataset with a CEO born in the 2000s, AnySphere (makers of Cursor). We excluded this data point because median values were only calculated for decades with at least three companies.

Platform shifts produce new generations of outsized founders. The 1980s cohort rode mobile and cloud. The early signal suggests the 1990s cohort will ride AI.

Each platform shift produces its own generation of founders.

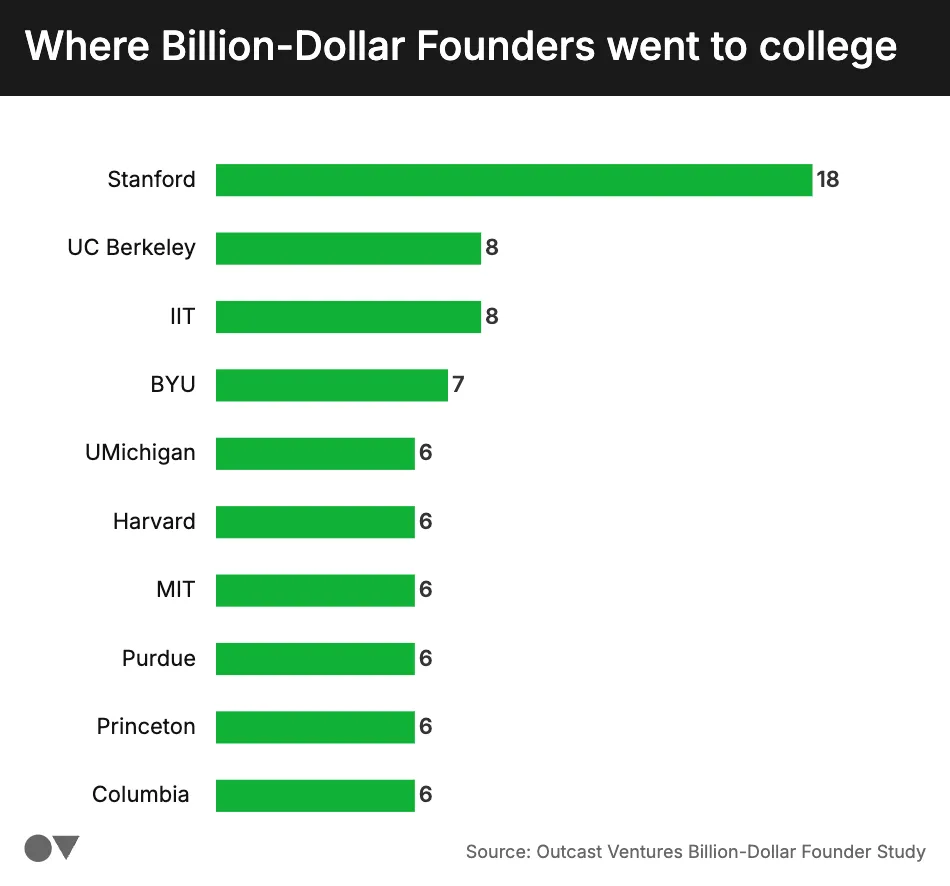

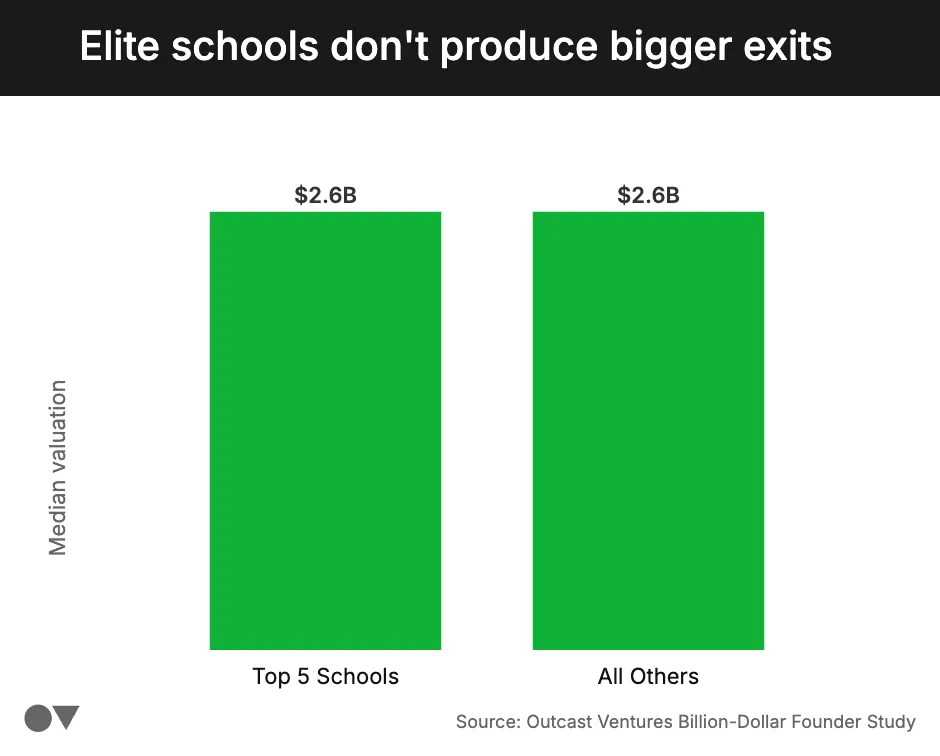

Elite schools produce founders, not bigger exits.

Certain institutions appear frequently among billion-dollar CEOs. Stanford leads. UC Berkeley and IIT follow. MIT, BYU, Michigan, Harvard, and others show up repeatedly.

Stanford clearly over-indexes in raw founder count, which is not surprising given their proximity to Silicon Valley, the density of venture capital, and strong peer networks.

Ilya Strebulaev’s research on over 3,200 unicorn founders, finds a similar concentration at the top, with Harvard, Stanford, and Wharton producing the most unicorn founders by raw count.

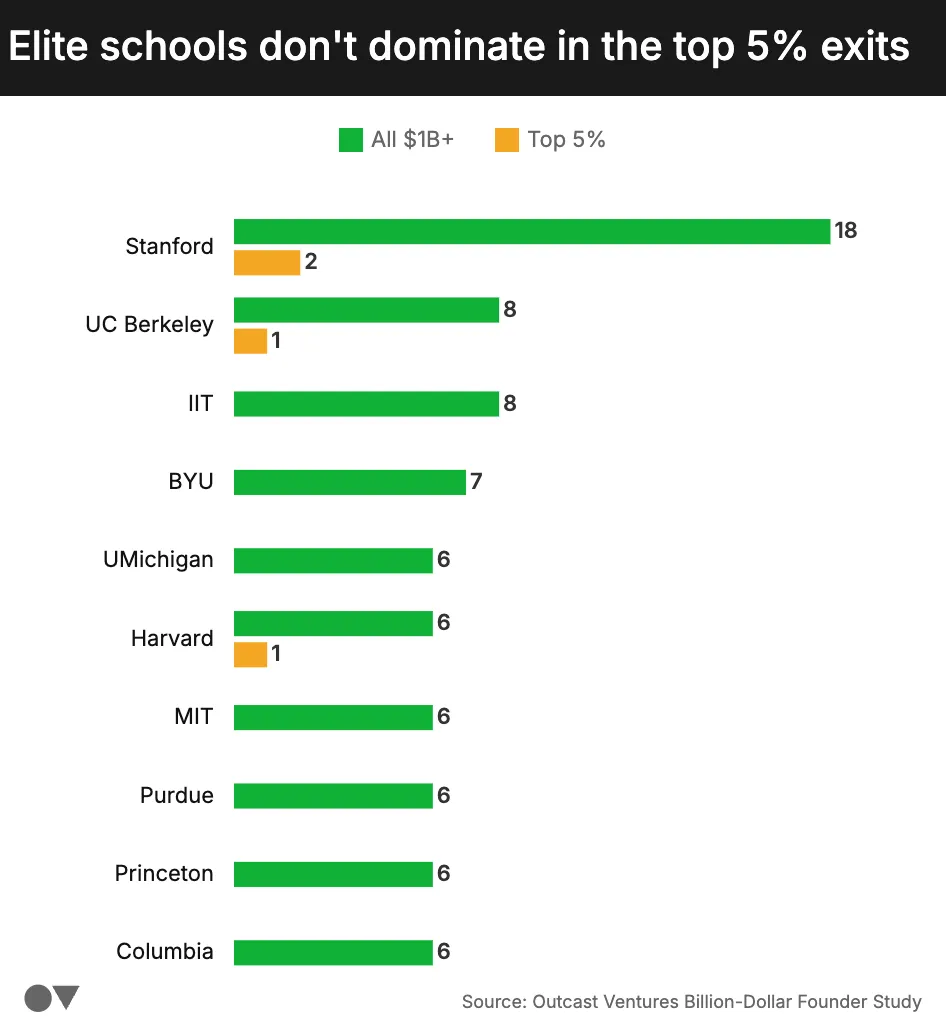

But raw count is only half the story. When isolating the top 5% of exits by valuation, Stanford shows up two times while many elite institutions do not appear at all.

There is mild concentration, but no monopoly. So does pedigree actually predict exit size?

Founders from the five most represented schools have a median exit valuation of $2.6B. And founders from every other school? Also $2.6B.

Elite schools are clearly overrepresented in founder counts. They increase exposure and access, but prestige does not determine the size of the exit. The ceiling is set by other variables like market timing, team structure, endurance, and how long a founder can keep building.

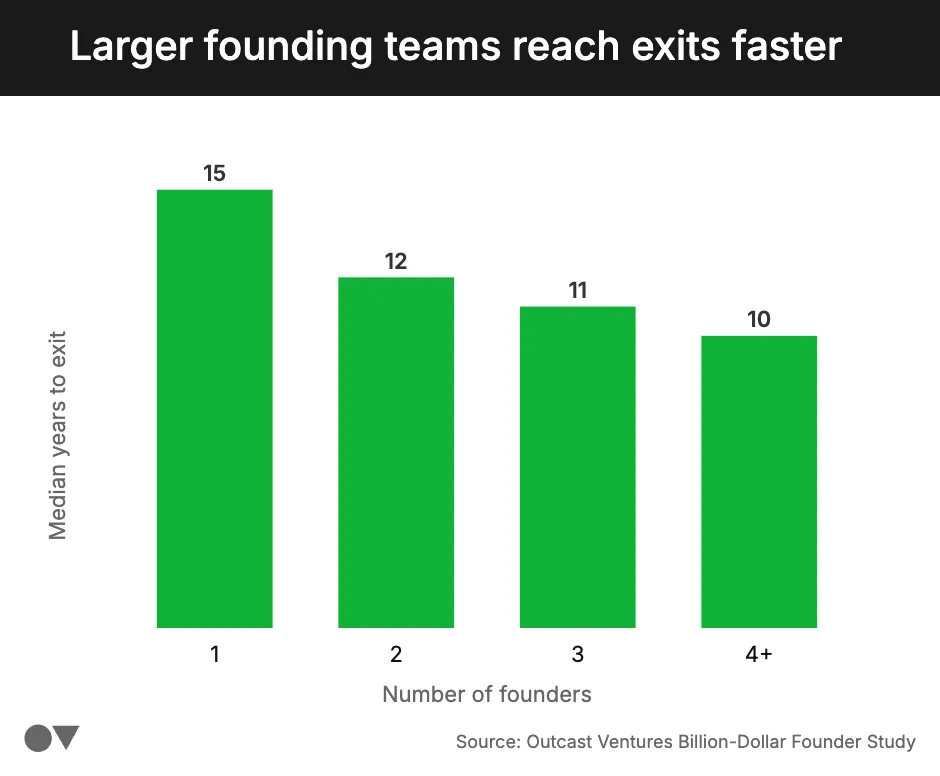

Solo founders take longer

One assumption about multi-founder teams is that coordination slows them down. More opinions. More conflict. More complexity.

However, reality tells a different story: that solo founders take the longest to reach liquidity.

The gap is large, with solo-founded companies taking roughly three years longer to reach a liquidity event.

Multi-founder teams don’t slow companies down. If anything, they compress the timeline.

Layer this onto earlier findings and the pattern becomes clearer. Solo founders are less common among billion-dollar exits, they nearly disappear in the top 5%, and they take longer to get there.

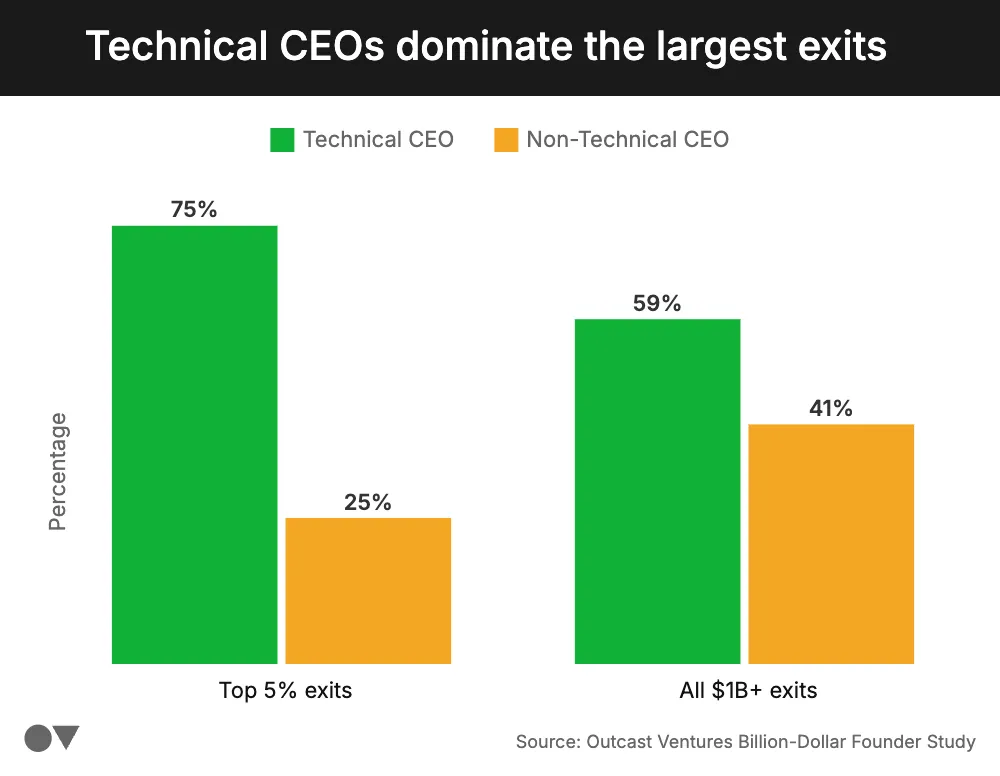

The technical CEO edge

There’s a long-running debate about whether companies need a technical founder in the CEO seat to build something large. Many iconic companies have been led by non-technical founders who excel at vision, storytelling, and sales.

But among the top 5% of exits, 75% of founding CEOs have a technical background, compared to 25% who are non-technical.

Technical founders start closer to the product. They can prototype quickly, iterate without waiting on others, and make better early technical decisions when teams and resources are limited, creating a significant advantage.

This doesn’t mean non-technical founders can’t build massive companies, but the data suggests that when it comes to the very largest outcomes, companies are far more likely to be led by founders who deeply understand the technology they’re building.

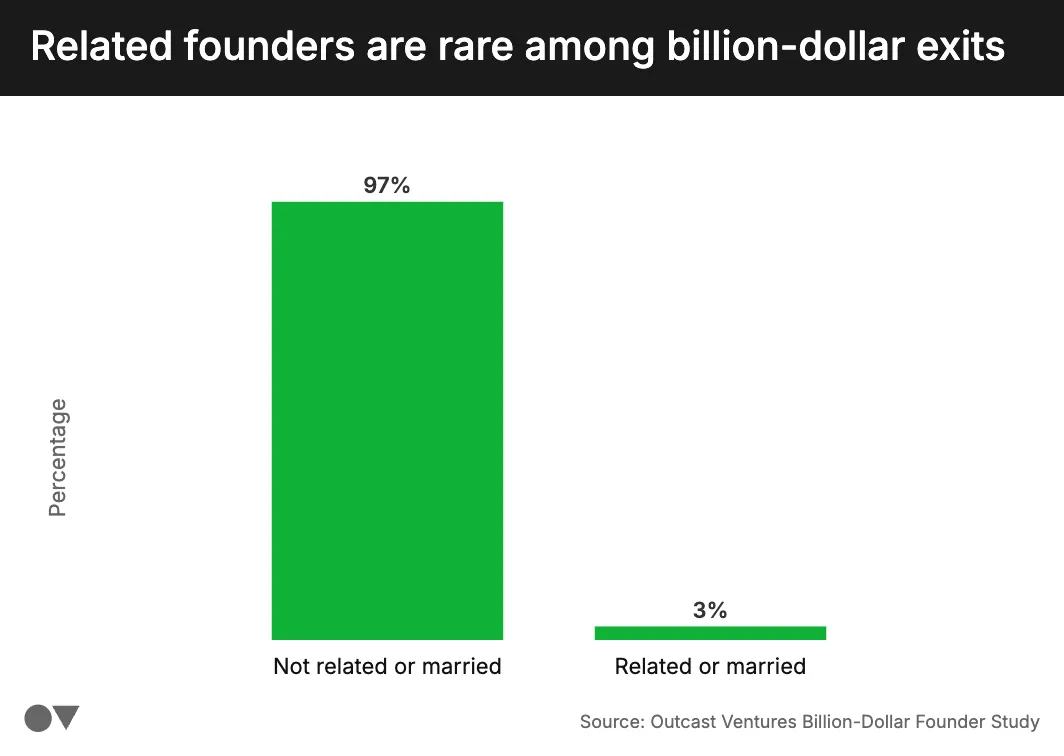

Family founders are extremely rare

Startup lore loves the story of family founders. Brothers starting a company in a garage. Married couples building something together. In practice, this almost never happens at venture scale.

Only 3% of companies in the dataset were founded by people who were related or married. The rest, roughly 97%, were built by founders with no family relationship. Trust clearly matters when starting a company. But that trust usually doesn’t need to come from family ties.

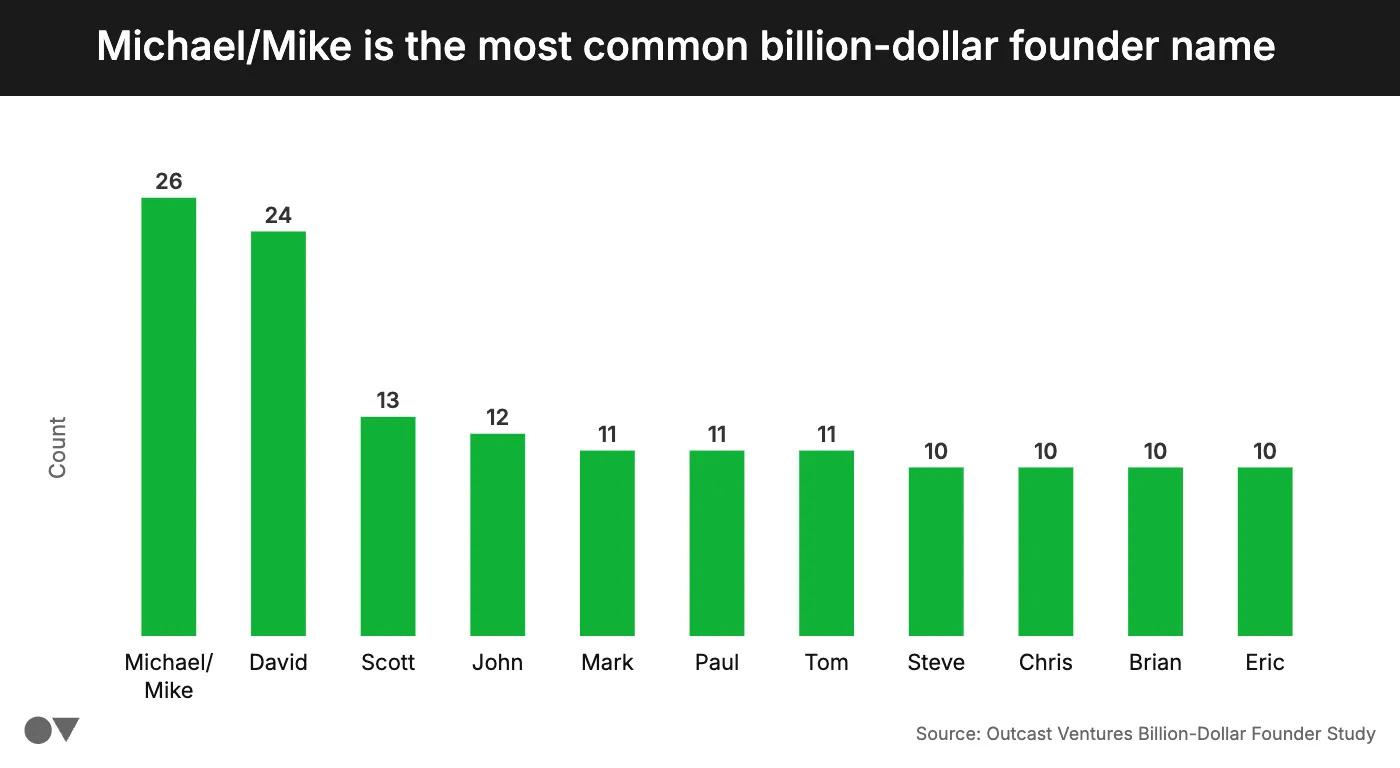

The most common Billion-Dollar Founder name Is… Michael/Mike

One of the fun things that falls out of a large dataset is the occasional pattern that almost certainly means nothing.

Founder first names are one of those.

So if your name is Michael or Mike, your odds of building a billion-dollar company appear unusually high, followed by familiar staples like David, Scott, and John.

Your name is not a growth strategy. More likely, it simply reflects the demographics of the founder population. Many founders in this dataset were born in the 1960s through 1980s, when a relatively small set of names dominated in the United States.

In other words, the startup ecosystem may be wildly innovative, but the names of the people building it are surprisingly conventional.

What actually predicts scale is the right team at the right time

Startup lore likes simple explanations: the brilliant solo founder, the college roommates who always knew they would build something together, or the prodigy who drops out of school and changes the world.

But when we look at the companies that actually make it to large exits, the pattern is more grounded. Successful companies are usually built by small, complementary teams. Their founders accumulate experience over a decade of building, and their timing aligns with major technology shifts.

What doesn’t matter as much – despite popular belief – is shared history. Founders who worked together previously produced lower median exit valuations, and going to the same school offered no measurable edge.

The best co-founder isn’t the most convenient one. It’s the most complementary one.

Billion-dollar outcomes come from structure and timing: the right founding team, the endurance to build for ten or more years, and the good fortune to start a company as a new platform wave begins.

If the earlier patterns hold, the next generation of outsized companies will likely follow the same formula. The difference is that the founders building them will increasingly be those who came of age alongside AI.

Methodology

To build this dataset, we started with two primary sources for identifying liquidity events. For IPOs, we used publicly available data compiled by Professor Jay Ritter at the University of Florida, which tracks U.S. IPO activity over time. For acquisitions, we relied primarily on PitchBook transaction data to identify venture-backed companies acquired for $1B or more.

From there, we applied a series of filters to construct a consistent universe of venture-backed technology companies. The companies had to be founded in the U.S., have a liquidity event between 2006 and 2025, and fall broadly within the technology sector. This includes categories such as consumer software, enterprise software, fintech, defense technology, hardtech, semiconductors, crypto, media, and telecom. We excluded sectors with unusual venture dynamics, such as biotechnology, pharmaceuticals, consumer packaged goods, and traditional consumer brands.

We also filtered out transactions that did not represent venture-style startup outcomes, including leveraged buyouts, private equity rollups, and companies that were already public but later taken private. For IPOs, we included traditional offerings as well as direct listings and SPAC mergers to capture the full range of modern public market entry paths.

For acquisitions, we used announced deal values combining both cash and equity consideration where available in order to approximate total transaction value.

All valuations were converted into 2025 dollars to allow comparisons across time. Rather than applying year-by-year CPI adjustments, we normalized earlier exits using the average U.S. inflation rate over the past twenty years (2.6% annually).

After applying these constraints, the dataset included just over 344 U.S. venture-backed companies that exited at $1B or greater.

Most of the founder-level data was assembled manually by reviewing LinkedIn profiles, podcast interviews, SEC filings, and historical articles to reconstruct how founding teams formed and what prior experience they had; this process allowed us to capture founder relationships and backgrounds that rarely appear in structured datasets.